Carbon Price Forecasting

Accurately forecasting the future economic costs of emissions is also very important both for companies and government agencies. This is important, for the following main reasons:

Having an accurate forecast over months and years into the future of the economic cost of emissions.

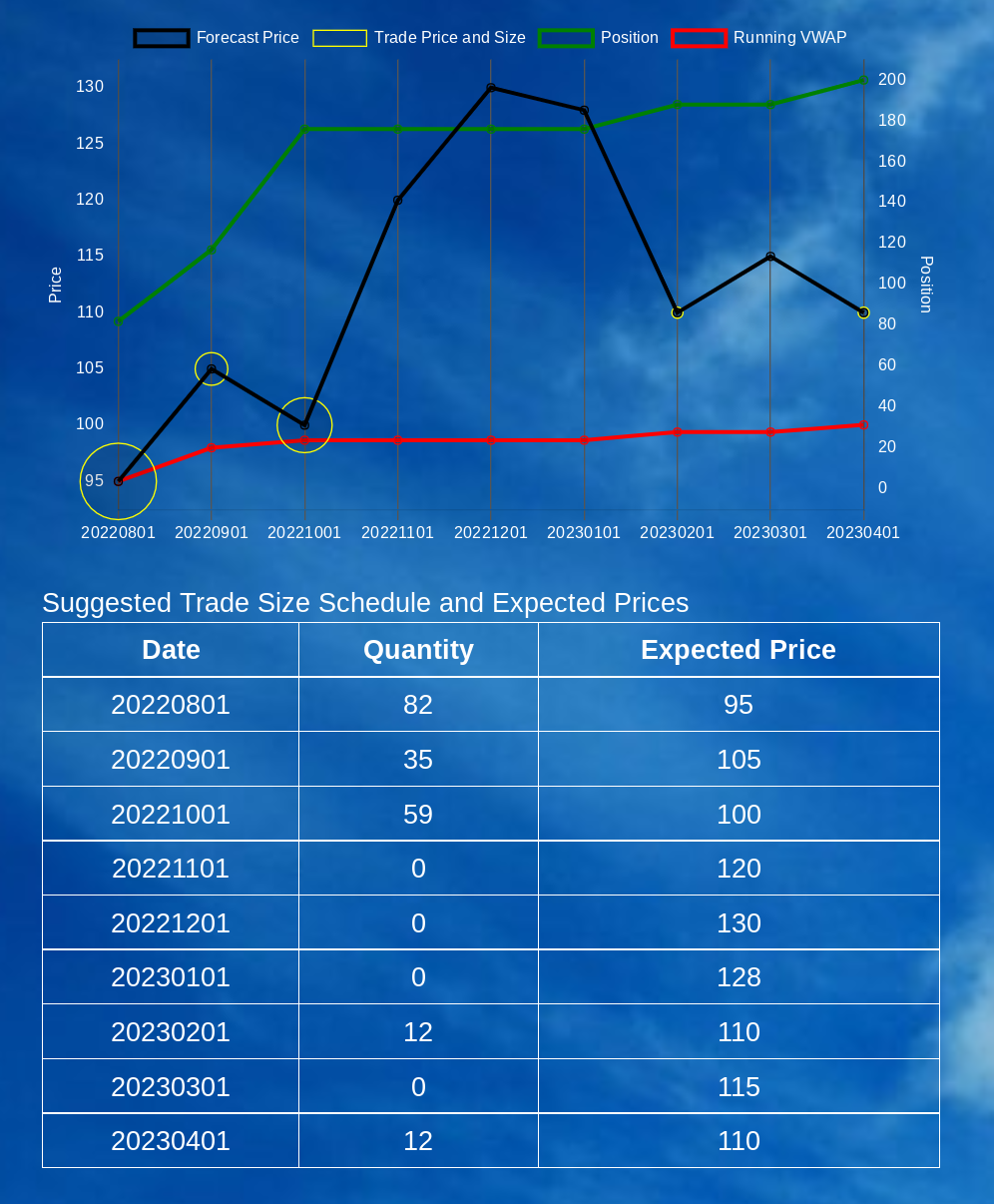

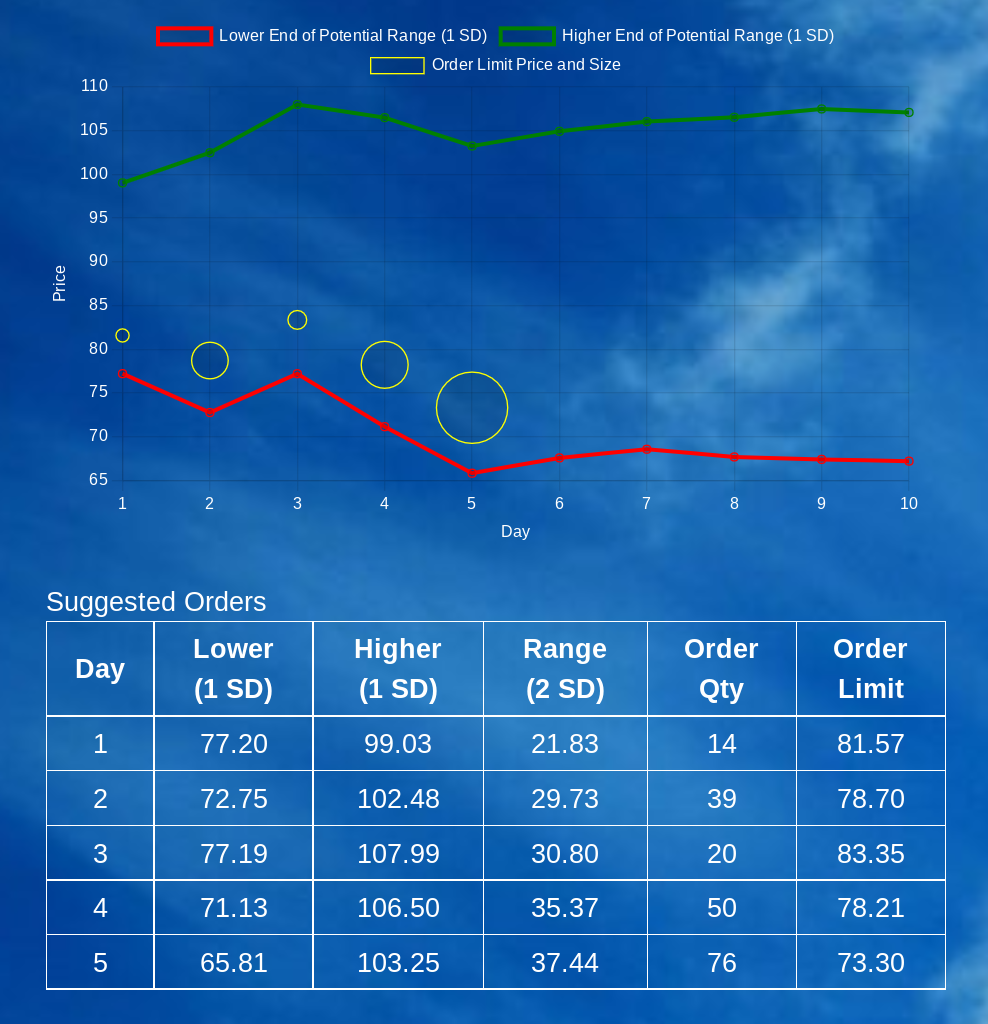

Having an accurate forecast, for trading tomorrow or over the next ten days, of how the traded carbon price is predicted to move, thus allowing buyers to optimise timing to reduce their VWAP and sellers to optimise timing to maximise their VWAP.

Helping covered entities plan their purchase, or sales, of carbon credits against their forecast emissions.

Helping importers who face (as now in the EU) a Carbon Border Adjustment Tax, where the tax rate tracks the EU ETS price, to better forecast their import tax bill (and purchase of certificates)

To help both companies and government agencies to better forecast the future price of traded carbon credits we have developed algorithms for predicting carbon prices as follows:

A large scale (8500 data sets) macroeconometric time series model to predict the short to medium term (from a month ahead to 3 years) market price of traded carbon credits. Our algorithm achieves a very high correlation (R2) and low average error (RMSE). Click to see the large scale forecast data.

A micromarket algorithm using 6 key market metrics to predict the trading price movements in the market (EU ETS or other ETS) for tomorrow and for ten days ahead. This has produced a high performance ratio with successful trades of about 75% of total. Click to see the micromarket forecast data..

Macro (long term) forecast, Buying at the optimal time

Macro (long term) forecast, Selling at the optimal time

Micro (short term) forecast, Buying at the optimal time

Micro (short term) forecast, Selling at the optimal time